Cash Basis Accounting vs. Accrual Accounting

When Is Accrual Accounting More Useful Than Cash Accounting?

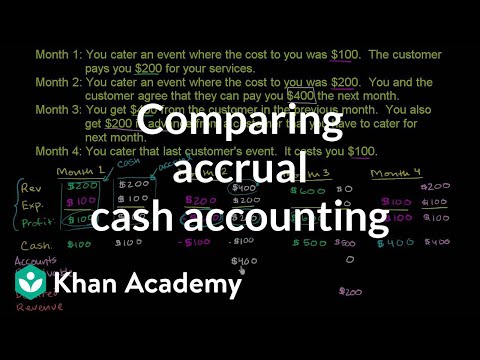

Accrual accounting is a method of accounting where revenues and expenses are recorded when they are earned, regardless of when the money is actually received or paid. For example, you would record revenue when a project is https://accountingcoaching.online/ complete, rather than when you get paid. The cash basis of accounting recognizes revenues when cash is received, and expenses when they are paid. This method does not recognize accounts receivable or accounts payable.

At his first meeting with Marilyn, Joe asks her for an overview of accounting, financial statements, and the need for accounting software. Based on Joe’s business plan, Marilyn sees that there will likely be thousands of transactions each year. She states that accounting software will allow for the electronic recording, storing, and retrieval of those many transactions. Accounting software will permit Joe to generate the financial statements and other reports that he will need for running his business. This concept is basically an accrual concept since it disregards the timing and the amount of actual cash inflow or cash outflow and concentrates on the occurrence (i.e. accrual) of revenue and expenses.

Reviso is a cloud accounting platform providing efficient online collaboration between small businesses and accountants. When accounting, provisions are recognized on the balance sheet and then expensed on the income statement. A supplier delivers goods at the end of the month, but is remiss in sending the related invoice. The company accrues the estimated amount of the expense in the current month, in advance of invoice receipt. A local lender issues a loan to a business, and sends the borrower an invoice each month, detailing the amount of interest owed.

By doing so, all expenses related to a revenue transaction are recorded at the same time as the revenue, which results in an income statement that fully reflects the results of operations. Similarly, the estimated amounts of product returns, sales allowances, and obsolete inventory may be recorded. These estimates may not be entirely correct, and so can lead to materially inaccurate financial statements. Consequently, a considerable amount of care must be used when estimating accrued expenses. Accrual basis is a method of recording accounting transactions for revenue when earned and expenses when incurred.

What is accrual basis of accounting with example?

Accrual basis is a method of recording accounting transactions for revenue when earned and expenses when incurred. A key advantage of the accrual basis is that it matches revenues with related expenses, so that the complete impact of a business transaction can be seen within a single reporting period.

This is more complex than cash basis accounting but provides a significantly better view of what is going on in your company. Accounting prepaid expenses method refers to the rules a company follows in reporting revenues and expenses in accrual accounting and cash accounting.

What Are the Objectives of Financial Accounting?

These principles are used in every step of the accounting process for the proper representation of the financial position of the business. Accounting principles are essential rules and concepts that govern the field of accounting, and guides the accounting process should record, analyze, verify and report the financial position of the business. Materiality Principle or materiality concept is the accounting principle that concern about the relevance of information, and the size and nature of transactions that report in the financial statements. Choose between two different trials, both containing all the core features of our accounting system. One of the trials is without data and can be upgraded to a subscription within the 14 days period.

The alternative method for recording accounting transactions is the cash basis. Business transactions are events that have a monetary impact on the financial statements of an organization. When accounting for these transactions, we record numbers in two accounts, where the debit column is on the left and the credit column is on the right.

You enter an accrued liability into your books at the end of an accounting period. In the online bookkeeping next period, you reverse the accrued liabilities journal entry after paying the debt.

What is the Accounting Method?

- Those are the people who start off on the wrong foot and end up in Marilyn’s office looking for financial advice.

- When the job is completed, you recognize the entirety of the $1,000 regardless of whether you have received the other half of the payment yet.

- These are usually the monthly financial statements most business managers are familiar with, such as the income statement and balance sheet.

The downside is that accrual accounting doesn’t provide any awareness of cash flow; a business can appear to be very profitable while in reality it has empty bank accounts. Accrual basis accounting without careful monitoring of cash flow can have potentially devastating Correlation consequences. With the accrual method, income and expenses are recorded as they occur, regardless of whether or not cash has actually changed hands. The sale is entered into the books when the invoice is generated rather than when the cash is collected.

Therefore, when you accrue an expense, it appears in the current liabilities portion of the balance sheet. We now offer eight Certificates of Achievement for Introductory Accounting and Bookkeeping. The certificates include Debits and Credits, Adjusting Entries, Financial Statements, Balance Sheet, Income Statement, Cash Flow Statement, Working Capital and Liquidity, and Payroll Accounting.

Accrued liabilities show goods and services that were delivered but not billed. To close your books, you must make an accrued expense journal entry. Accrued expenses can reveal how debts affect the business bottom line before receiving adjusting entries bills. During everyday operations, you buy goods and services for your business. To organize expenses and keep your small business cash flow on track, you might need to record accrued liabilities in your accounting books.

Materiality Principle in Accounting: Definition

And you’ll need one central place to add up all your income and expenses (you’ll need this info to file your taxes). Many small businesses opt to use the cash basis of accounting because it is simple to maintain. It’s easy to determine when a transaction has occurred (the money is in the bank or out of the bank) and there is no need to track receivables or payables. The cash method may be appropriate for a small, cash-based business or a small service company. You should consult your accountant when deciding on an accounting method.

What is materiality principle?

Accrual concept is the most fundamental principle of accounting which requires recording revenues when they are earned and not when they are received in cash, and recording expenses when they are incurred and not when they are paid.

You can think of cash basis accounting similarly to your checkbook register – at the end of the month, you balance everything to see how much cash you have in the bank. Many companies can choose which method they want to use depending on the needs of their business. The real difference between the two is the timing of when your company accounts for its expenses and revenue earned.

By requiring businesses to book revenue when earned and expenses when incurred, GAAP aims to prevent companies from misrepresenting their business activity by manipulating the timing of cash flows. Under cash accounting, a business could avoid recording a loss for, say, the month of June simply by holding off on paying its bills until July 1. If September looks like it’s going to be a weak month for sales, a company could prop up the numbers by delaying the billing of some customers so that their payment doesn’t arrive until after Sept. 1. With accrual accounting, a company hoping to manipulate its numbers like this would have to lie about the timing of revenue and expenses — in other words, to commit fraud. If you plan to seek outside financing for your business at some point, then the accrual accounting method is most likely your best bet.

Accrued liabilities recognize any unrecorded expenses incurred but not billed. Both accrued expenses and accounts payable are current liabilities, meaning they are short-term debts to be paid within a year. AccountDebitCreditCash AccountXAccrued Liability AccountXWhen the original entry is reversed (showing you paid the expense), it’s removed from the balance sheet.

Step 1: You incur the expense

Establishing how you want to measure your small business’s expenses and income is important for financial reporting and tax purposes. However, your business must choose one method for income and expense measurement under tax law and under U.S. accounting principles.

This example displays how the appearance of income stream and cash flow can be affected by the accounting process that is used. The cash method is also beneficial in https://accountingcoaching.online/blog/accounting-for-bonds-payable/ terms of tracking how much cash the business actually has at any given time; you can look at your bank balance and understand the exact resources at your disposal.